Acquisitions have created the lowest true cost filtration suppliers

A good product customized for an application is better than a great product which has not been adapted. The lowest true cost is a function of use and not just potential. With the new uses of digital intelligence, a good filter can be replaced as warranted whereas a great filter can cause all sorts of problems if it’s not replaced at the right time.

The inventor of a product is challenged to develop the application knowledge and the support structure to assist the customer to maximize performance. The result is that over time the company is acquired by a larger entity.

Total Cost of Ownership Factors

The acquisition of the innovating companies has been typical in the filtration industry.

In 1956, Tom Reinauer of Pulverizing Machinery (later MikroPul) tackled the operational problems of shaking bags to reduce accumulated dust in collectors used in pulverizers. He invented pulse jet cleaning. It was such an improvement that over time it became the method of choice. The true cost was so much less and the patent position so strong that a licensee, Hosokawa, in Japan earned profits large enough to acquire the U.S company.

Today, MikroPul is part of the Nederman Company. The success of this company is in a large part due to the reduction in the cost of capturing the polluted air. The cost of dust collection is directly proportional to the amount of air to be cleaned and not the amount of dust to be removed.

In retrospect an individual in an OEM user company invented pulse jet cleaning. This resulted in a very profitable dust collector company. But patents expired. The company then became part of an international group which distinguishes itself by understanding the dust problems and providing solutions.

Regulations can quickly change cost of ownership factors. The rigid frame versus wire and weight collection electrodes in an electrostatic precipitator is an example of new technology quickly replacing the old. At the time of the 1979 Clean Air Act, Research Cottrell and Western Precipitation dominated the U.S. precipitator market. Their licensees dominated the world market. The 1979 Clean Air Act introduced the requirement for continuous compliance not just on initial installation. Wire and weight designs of Western and RC were easily broken and could not meet the continuous requirement. Very shortly Flakt from Europe became the largest U.S. supplier with its rigid frame design.

The lesson here is that external forces such as regulations can quicky change the total cost of ownership. Companies need to be anticipating these forces and to adapt. International companies can best pursue the regulatory changes which typically start in country and then are copied by others.

Patents and even technology can be forgotten. The venturi scrubber was patented in the 1890s in Austria for town gas pollution control. It was reinvented in 1945 in the U.S. An improved variation was invented in the 1960s and then reinvented within the last decade. Pollution control innovations soar when regulations create big new markets. But they shrink when when regulations are met. The experts retire and much knowledge is lost.

Dean Spatz launched Osmonics in 1969. He started by rolling reverse osmosis (RO) membranes in his garage. He was at the forefront of filtration technologies to remove small particles continuously. The company was sold to GE in 2002 when revenues had risen to over $200 million. GE then sold its water group to Suez. This new parent offers complete solutions. It supplies treatment equipment but also is a third party operator of municipal water and wastewater plants around the world. Suez can remotely monitor these plants and optimize processes such as RO.

The lesson here is that the lowest true cost involves the whole process and not just an aggregation of individual equipment costs. Equipment suppliers can team with digital intelligence companies or acquire them and offer packages.

3M changed the residential air filter market in the 1990s when it developed a low pressure drop high-efficiency media by creating an electrostatic effect. By 2005 it had built a billion dollar business. It then bought a liquid filtration company, Cuno, for $1.35 billion.

Frank Donaldson built the first tractor air filter in 1915 and created the Donaldson Company, which became the leader in filters for off road equipment. In 1974 it bought Torit, a dust collector company. What was unique was the use of compact, cellulose cartridges rather than conventional bags. For light dry dust applications the cost of ownership was less. Donaldson is now the world leader in small modular dust collectors.

Donaldson is moving to expand its base with two recent acquisitions of liquid filters and process technology in the biopharmaceutical field.

It has been 52 years since Bob Gore discovered expanded PTFE and changed the fortunes of the company started by his father. W.L. Gore and Associates has expanded membrane technology into many new areas, including gas, as well as particle separation. The philosophy is to sell unique products. When patents expire or markets change they may move on to greener pastures.

Gore is research oriented and continues to develop new products. It has made relatively few acquisitions. Today, with $3.8 billion in annual revenues, the enterprise is privately owned. More than 11,500 employees (called Associates) worldwide are also part owners of the enterprise through the Associate stock ownership plan.

The fact that Gore stands out for its technology approach and lack of acquisitions is likely a result of the ownership structure. This approach can yield a high EBITA and ROI.

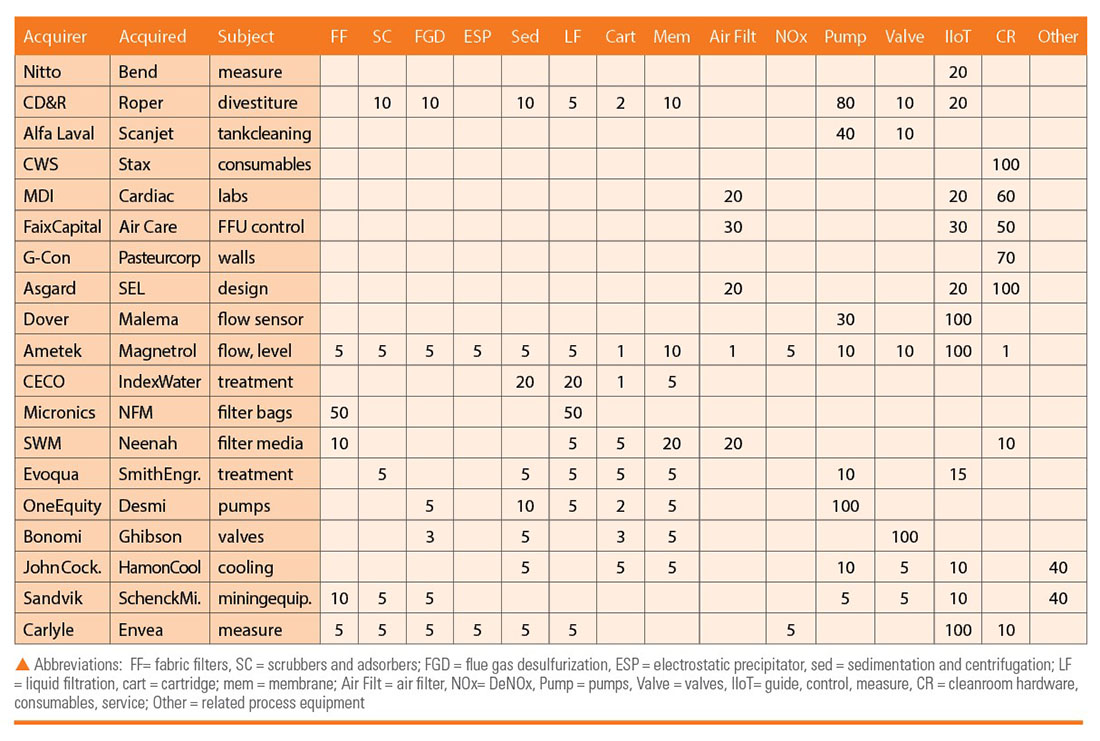

In order to best evaluate any company it is desirable to analyze the acquisitions. The information about financials and goals in a niche market is likely to be revealed only at the time of acquisition. McIlvaine maintains a database with over 1000 acquisitions in air, water, and energy.(1) Dozens of new acquisitions are added each month. Many reveal the synergy between flow measurement and various treatment technologies. These synergies are represented by percentages. A flow measurement company would have 100% in IIoT, but if 10% of the use is with liquid filtration equipment that percentage will also be included.

The synergy low is 20% where the acquired measurement company is mostly focused outside the target area. The high is 173% for a measurement acquisition tied closely to filtration and separation.

In order to provide the lowest true cost the supplier has to evaluate each of the competitor’s products. The acquisition history is an important resource. For a multi-product company or private equity firm looking for the next best fit, the acquisition histories of the participants are a good starting point.

(1)Air/Gas/Water/Fluid Treatment and Control: World Market published by the McIlvaine Company

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}